/ New Maximum TERs for Chilean Pension Fund investments. Further drops expected next year.

July 6, 2020Period July 1, 2020 to June 30 2021.

Nicole Cartier, senior associate

Felipe Cousiño, partner

Annually, the Chilean pension regulator (Superintendencia de Pensiones– “SP”) jointly with the Chilean securities, banking and insurance regulator (Comisión Para El Mercado Financiero – “CMF”) sets the maximum fees and expenses (“Max TER”) that Chilean pension fund managers (“AFPs”) can pay in respect of the investments they hold in funds (including foreign funds) on behalf of the pension fund portfolios they manage. To the extent the fees and expenses of a fund that an AFP has invested in exceed the Max TER, the AFP is required to reimburse the pension fund the excess (i.e. not out of the pension fund assets).

The CMF jointly with the SP have published on July 1st the terms for Max TERs effective from July 1, 2020 to June 30, 2021 (“TER rule”). The new TER rule appears to impose reduced fees on registered funds, while imposing more stringent terms on private funds, notwithstanding that rates for the latter remain unchanged.

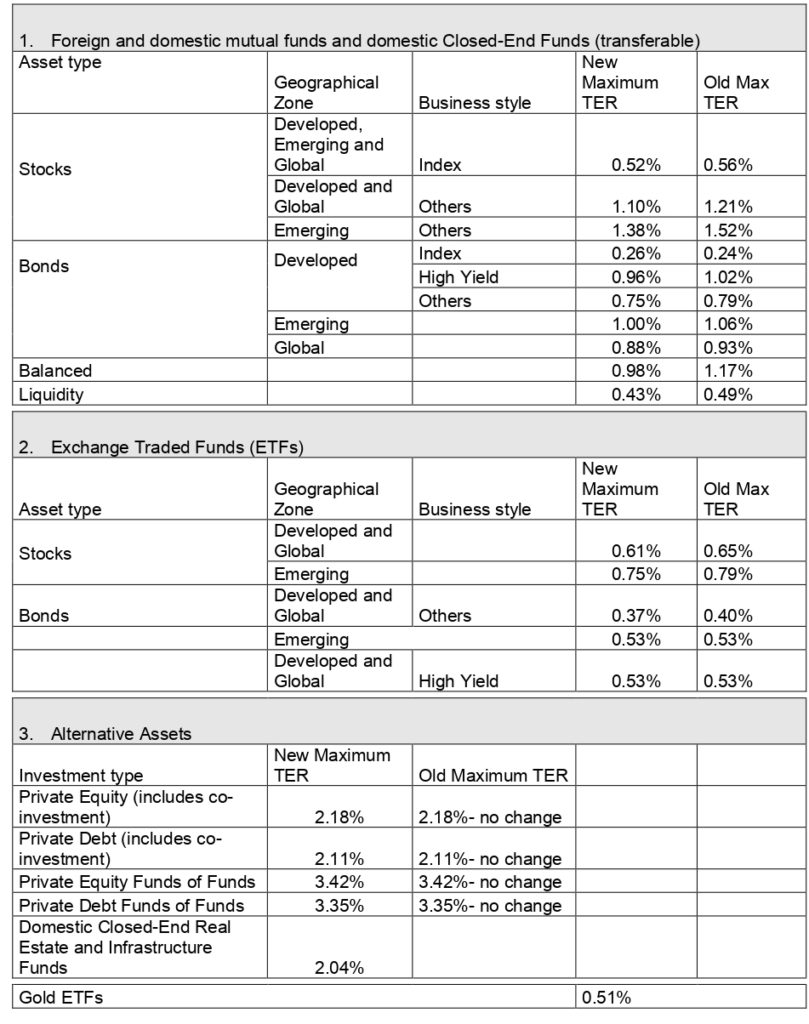

Indeed, in relation to mutual funds, registered closed ended funds, ETFs and alternative/private funds the Max TER rates will vary (or not vary) as follows:

The new Rule clarifies that domestic private debt funds will have the same Max TER as foreign private debt funds, thus creating a level playing field between these two categories. It must be noted that domestic private debt was recently introduced into the Chilean pension fund investment regime and was characterized as forming part of the alternative asset bucket of investments.

Another new asset type that is subject to the Max TER is that of Gold ETFs, which were also recently introduced as an eligible investment.

One improvement in terms applicable to private funds is that private equity and private debt feeder funds will now be allowed to calculate their TERs based on the same frequency as the underlying master funds. This is welcome relief given it reduces costs associated with feeder funds.

Some clarification was introduced to the part of the Max TER rule that allows amortization of past and future expenses over the remaining life of the fund (i.e. the original term of the fund, not fund term extensions) if these are expenses that, due to their nature, should be distributed over more than one period. The rule now specifies that eligible expenses will only be those related to the structuring or to the investments of the relevant vehicle.

However, not all is good news for private equity and private debt funds. Indeed, additional fees charged to Chilean pension funds for investing in alternative funds after the first close will have to be borne by the relevant AFP. In practice this means that an AFP will not invest after the first close if it will be charged an additional or penalty fee. Furthermore, though the text of the new rule is unclear, AFPs would also have to bear the excess TER over the one informed at the time of subscription of commitments if the pension fund, having entered the fund after the first close, is required under the LPA to bear expenses incurred prior to the first close. These will probably be new matters for discussion in side letters to limited partnership agreements.

The drop in the caps on fees is explained in part by a change in the methodology to calculate the Max TERs. A further change will be applicable next year which may lead to further drops. Indeed, for registered funds there has been a transition from the 90th percentile to the 75th percentile (which is an average between 90 / 75) relating to TERs found in the Morningstar Direct United Sates Mutual Funds as at May 2020 data base, causing the reduction of the Max TERs this year. Next year the Max TER of registered funds will be based on the 75th percentile only, so there may be another drop for the 2021-2022 period. The drop will of course depend on where the market moves as captured in the applicable databases that will be used next year (possibly the ones as at May 2021). However, this change in methodology will not apply to alternative funds (private equity, private debt, infrastructure and real estate) and Gold ETFs whose Max TERs shall continue to be calculated on the basis of the 90th percentile of the TERs contained in the relevant most recently available databases (this year the ones used were Prequin Private Capital Fund Terms Advisor 2018, Morningstar Direct United states Mutual Funds – for infra and real estate- and Bloomberg as at May 2020- for Gold ETFs).

If you need more information, please do not hesitate to contact our capital markets team.